Reviewed By: Student Renter Editorial Staff

Sending your child off to college is a major milestone. As a parent, you’re probably thinking about tuition, campus safety, and whether they’ll remember to do their laundry. One thing that often gets overlooked? What happens if their laptop is stolen, their dorm floods or their off-campus apartment is broken into? That’s where student renters insurance comes in.

Student renters insurance is a simple, affordable way to help protect your student’s personal belongings while they’re away at school. Whether your child is living in a dorm, an apartment, or a shared house, renters insurance can provide peace of mind in the event of theft, fire, water damage, or liability issues.

Many parents assume that their homeowner’s insurance will cover their child at college. Sometimes, that’s true, but only in very specific situations and often with limited coverage.

For example, some policies only protect students who live in on-campus housing and are still listed as dependents at the same address. If your student is renting an apartment off campus, they likely need their own policy.

This guide was created to help you understand exactly what student renters insurance covers, how much it costs, and how to choose the right policy before move-in day. We’ll walk through common questions parents have, explain how coverage works in different living situations, and point out potential mistakes to avoid.

Our goal is to keep things clear and practical, with no confusing jargon or pressure to buy anything. These are just straightforward answers to help you protect your student’s belongings and give you more confidence as they head into this new chapter of life.

Let’s get started.

What Every Parent Should Know About Renters’ Insurance

What is renters’ insurance?

Renters’ insurance is a type of policy that helps protect a tenant’s personal property in case of theft, fire, certain types of water damage, or other covered events. It can also provide personal liability coverage if the renter accidentally damages someone else’s property or causes an injury. For college students, this means coverage for items such as electronics, furniture, clothing, and even dorm room or apartment-related mishaps.

Unlike homeowners insurance, which covers both the structure and the contents of a home, renters insurance covers only the contents and liability. The building itself is the responsibility of the landlord or property owner. For students, renters insurance steps in to help when something goes wrong that affects their belongings or their legal responsibility as a tenant.

Do college students need renters insurance?

While renters insurance is not always required, it is strongly recommended. College students often bring valuable items to school: laptops, phones, bikes, textbooks, and more. These items can be easily lost, damaged, or stolen, especially in shared or high-traffic living spaces.

Renters insurance helps reduce the financial burden if something unexpected happens. It is beneficial for students living off campus in apartments or shared housing, where the landlord’s insurance does not extend to tenant belongings. Even students in dorms may benefit, depending on whether their parents’ homeowner’s policy offers adequate coverage.

Does my child need renters insurance in a dorm?

That depends on your existing homeowner’s policy. Some policies may extend limited coverage to a student living in an on-campus dorm, as long as the student is a dependent and maintains legal residence at your home address. However, that coverage may be limited by distance, dollar amount, or type of claim.

Even when there is some extended coverage, it may come with a high deductible or restrictions on what is covered. In many cases, it is easier and safer to purchase a separate student renters insurance policy to ensure full protection and a smooth claims process.

Also Read: Dorm Room Insurance vs. Renters Insurance

Is renters insurance required by colleges or landlords?

Colleges generally do not require students to carry renters insurance, though they may recommend it. However, some off-campus landlords do require it as part of the lease agreement. This is especially common in private apartments and student housing complexes.

If renters insurance is required, it will usually need to meet minimum coverage amounts and list the landlord or property manager as an additional interest. This ensures the landlord is notified if the policy is canceled or changed.

What does renters insurance cover for students?

Most renters insurance policies for students include three key types of coverage:

- Personal property – Covers belongings like electronics, furniture, clothing, books, and valuables in case of theft, fire, smoke damage, certain water leaks, vandalism, and more.

- Liability protection – Covers accidental damage to someone else’s property or if someone is injured in your child’s rental space.

- Loss of use – Covers temporary housing costs if their unit becomes unlivable due to a covered event.

Optional add-ons (also called riders) may be available for items like expensive electronics, jewelry, or musical instruments.

Also Read: What Does Student Renters Insurance Not Cover? Exclusions Every Parent Should Understand

How much does student renters insurance cost?

Renters insurance for college students is usually very affordable. On average, it costs between $5 and $15 per month. The exact cost depends on factors such as the coverage amount, deductible selected, provider, location, and whether the student lives in a dorm or off-campus apartment.

Most providers offer basic plans with flexible limits and the ability to customize coverage depending on needs. Some also offer student-specific plans or discounts for bundling with auto insurance.

Also Read: How Much Renters Insurance Coverage Does a Student Actually Need?

Does renters’ insurance cover laptops and textbooks?

Yes, renters insurance typically covers laptops, tablets, and textbooks under the personal property section of the policy. However, coverage may only apply if the item was stolen or damaged due to a covered event, such as theft or fire.

Accidental damage (such as dropping a laptop or spilling coffee on it) is generally not covered unless the policy includes an add-on or endorsement for electronics protection. It is important to check the limits and exclusions related to high value items to make sure coverage is sufficient.

Can parents pay for renters insurance on behalf of their student?

Yes. In most cases, a parent can pay for their student’s renters insurance policy, even if the student is the named insured. Many insurance companies allow flexible billing options, including online payment, automatic renewal, and billing to a parent’s email or credit card.

It is common for parents to manage the initial setup of the policy and then turn over control to the student once they are more comfortable handling their own expenses.

Will my homeowner’s insurance cover my student’s dorm?

Sometimes. If your student is living in a college dorm and is still considered your dependent, your homeowner’s policy may extend partial coverage. This is often limited to a percentage of the total personal property coverage, such as 10 percent, and may only apply while the student resides in an on-campus residence.

There are also distance limitations in some policies.

For example, if the student’s dorm is located more than 100 miles from your primary residence, coverage might not apply.

Additionally, claims filed under your homeowner’s policy could impact your own insurance record, which is another reason why many families opt for a separate renters policy.

How do I buy renters’ insurance for a student?

Buying renters’ insurance for a student is simple and can be done online in minutes. Here are the general steps:

- Choose a provider – Compare options based on coverage, cost, and customer reviews.

- Enter the student’s address – Specify whether it is a dorm, apartment, or other housing.

- Select coverage limits – Choose how much personal property and liability coverage is needed.

- Set the deductible – This is the amount the student will pay out of pocket before coverage applies.

- Add optional riders – Include any extra protection needed for electronics, jewelry, or bikes.

- Review and pay – Set up payment details and choose who will receive policy notices.

Most major insurance providers offer renters insurance suitable for college students, and many allow parents to manage the account on behalf of their child.

Policy Details Most People Miss

What is the typical deductible for student renters insurance policies?

The deductible is the amount your student will pay out of pocket before insurance coverage kicks in. For most student renters insurance policies, the typical deductible ranges from $250 to $1,000. A lower deductible usually means a slightly higher monthly premium, while a higher deductible can reduce the cost of the policy.

When choosing a deductible, it is good to consider how much your student could realistically afford to pay in an emergency. If their laptop is stolen or a fire damages their belongings, the deductible amount is what they must cover before insurance will reimburse the rest.

How is coverage different for named insured vs. additional insured?

A named insured is the person listed as the primary policyholder. This person has full rights under the policy, including the ability to make claims, change coverage, or cancel the plan.

An additional insured is someone else listed on the policy, usually for notification purposes. In the student housing world, landlords or housing complexes are often listed as additional insured or “interested parties.“ This means they get notified if the policy lapses or changes, but they are not covered by the policy.

For roommates, only those listed as named insureds are protected by the renters insurance. If your student’s name is on the policy but their roommate’s is not, the roommate’s belongings will not be covered.

Does renters insurance cover damage from roommates?

Renters insurance does not typically cover damage caused by a roommate unless that roommate is also listed as a named insured on the policy. Each person is responsible for their own belongings and liability unless otherwise agreed upon in a shared policy.

For example, if your student’s roommate accidentally sets off a kitchen fire that damages your student’s belongings, your student may still be able to file a claim under their own policy if the event is considered accidental and covered.

However, coverage will vary depending on the policy terms and how the incident occurred.

Encouraging each roommate to carry their own renters insurance is the best way to ensure everyone is properly covered.

Are bicycles or scooters covered under renters insurance?

In most cases, bicycles and electric scooters are covered under the personal property portion of a renters’ insurance policy. Coverage typically applies if the item is stolen or damaged by a covered event, such as fire or vandalism.

However, there are some limitations. Most policies require that the bike or scooter was stored securely (such as being locked) in order for theft to be covered. There may also be limits on the reimbursement amount. If the bike or scooter is particularly valuable, your student may need to add a rider or schedule it separately for full protection.

Accidents that happen while riding, such as a collision or damage to someone else’s property, may fall under liability coverage, but only in limited cases. Renters’ insurance is not a substitute for auto or personal injury coverage when operating motorized scooters.

Does renters insurance cover student housing off-campus?

Yes, renters’ insurance is commonly used by students living off-campus. Once your student signs a lease or rental agreement for an apartment or house near campus, they become responsible for protecting their own personal belongings and any accidental damage or liability.

Unlike dorms, off-campus housing is not connected to any parental homeowner’s policy, so it is almost always necessary to have separate renters insurance. Coverage works the same way as it does for any other renter, with protection for personal property, liability, and loss of use.

Make sure the address of the off-campus residence is correctly listed on the policy to ensure coverage applies.

Also Read: Renters Insurance for Off-Campus Student Housing: What to Know

Can roommates share a renters insurance policy?

Some insurance providers allow roommates to share a renters insurance policy, but it comes with risks. Shared policies require that all roommates be listed as named insureds. If one person is not listed, their belongings and liabilities are not covered.

Even when allowed, sharing a policy can complicate things. If there is a claim, the payout may be split or issued to just one policyholder. Any disputes between roommates about ownership or responsibility can create issues during the claims process.

For simplicity and accountability, it is often better for each roommate to have their own renter’s insurance policy. This allows for individual customization, separate claims, and clear lines of responsibility.

Also Read: Can My Child Share Renters Insurance with Their Roommate?

Does renters insurance follow a student who moves mid-semester?

Yes, but only if the policy is updated. If your student moves to a new apartment, dorm, or sublet, the renter’s insurance policy does not automatically carry over unless the address is changed with the insurance provider.

Failing to update the address may result in a claim being denied. Most providers allow address changes to be made easily online or by phone. Some even allow scheduled move dates in advance to prevent gaps in coverage.

If your student is moving between terms, cities, or types of housing, make sure their policy stays accurate so there is no lapse in protection.

Is renters insurance valid for short-term sublets?

Renters’ insurance may or may not cover a short term sublet. It depends on the provider and the terms of the policy. Some insurance companies allow temporary address changes or extend coverage to new locations as long as the student still holds the policy.

Others may not cover sublets at all or may require that the student has a legal right to occupy the space under a written agreement. In cases where the student is subletting from another person and is not on the lease, coverage could be denied.

Before your student moves into a short-term rental or sublet, contact the insurance company to confirm how coverage applies. In some cases, a new short-term policy may be needed.

Does it cover summer storage units?

Renters insurance may or may not cover personal belongings kept in a storage unit during the summer. Some policies extend coverage to off-site storage, but usually with a lower limit, often around 10 percent of the total personal property coverage.

For example, if your student’s policy covers $10,000 worth of belongings, they may only have $1,000 in coverage for items stored off-site. This can leave valuable items at risk if the unit is broken into or damaged by fire or flood.

If your student plans to store items over the summer, it is worth checking the policy details. In some cases, a separate storage insurance policy or rider can be purchased to ensure full coverage.

Also Read: Student Storage Insurance Guide

Can renters insurance be paused or canceled during breaks?

Renters insurance cannot typically be paused in the way streaming services or subscriptions can. However, the policy can be canceled if your student will not need it during the summer or an extended break.

Keep in mind that canceling the policy means losing coverage for any items stored in their apartment or storage unit. It also resets the policy history, which may impact discounts or eligibility later.

Some families choose to keep the policy active year-round, especially if the student’s belongings remain in place or if coverage is needed for liability reasons. Others cancel and reopen the policy when school resumes. Either option is valid. It just depends on the situation and the provider’s rules.

Advanced FAQs for Smart Parents

How fast can a student file a renters’ insurance claim?

Students can typically file a renters’ insurance claim online or through a mobile app within minutes of the incident. Most major insurance providers offer digital platforms that allow policyholders to upload photos, provide a description of the loss, and track the progress of the claim in real-time.

Once a claim is submitted, the processing time can vary. For straightforward claims like stolen electronics or minor water damage, some providers process and payout within one to three business days. More complex claims may take longer depending on the investigation, documentation, and whether third-party verification is required.

Encourage your student to report incidents quickly, keep receipts or proof of ownership when possible, and document damage with clear photos. These steps can significantly speed up the process.

What does personal liability coverage include?

Personal liability coverage helps protect your student financially if they are found legally responsible for damaging someone else’s property or causing accidental bodily injury. It can also cover legal defense costs, even if the student is not found at fault.

Examples include:

- A visitor slipping and getting injured in their apartment

- Accidental damage to a neighbor’s unit, such as a water leak

- Knocking over an expensive item while visiting someone else’s home

This coverage typically applies whether the incident happens inside the rental unit or elsewhere, as long as it involves the student’s personal actions or negligence. It does not cover intentional harm, business-related activities, or liability from driving.

Is alcohol-related damage at student parties covered?

In most cases, renters insurance will not cover damage or liability resulting from alcohol-related incidents, especially if laws were broken. This includes property damage or injuries that occur at a party where underage drinking takes place.

If your student hosts a gathering and someone gets hurt or causes damage while intoxicated, the insurance company may deny the claim.

Some policies have specific exclusions related to alcohol and controlled substances. Additionally, if the student is found to have acted negligently or violated local ordinances, coverage may not be applicable.

It is important to talk to your student about responsibility and how renters insurance works in real-world situations. Coverage is designed for accidents, not illegal or reckless behavior.

Does renters insurance cover studying abroad?

Most standard renters insurance policies do not automatically cover international locations. If your student is studying abroad, coverage may be limited or unavailable, depending on the provider and destination country.

Some insurance companies offer optional global coverage or international riders for students traveling overseas. These policies may cover theft or loss of belongings while abroad, but often exclude liability or damages caused in international settings.

Before your student heads out for a semester abroad, check with the provider to see what is included and whether a travel insurance or international renters insurance policy is necessary. In many cases, separate insurance will be required to provide full protection outside the United States.

Also Read: Renters Insurance for Study Abroad

Can renters’ insurance be bundled with auto or health?

Renters’ insurance can often be bundled with auto insurance, but not with health insurance. Many large insurance companies offer bundling discounts when your student holds more than one policy, such as renters and car insurance.

Bundling can save money and streamline billing. It also provides the convenience of managing all policies through one company.

Health insurance, however, is a completely different category and cannot be bundled with property or casualty insurance. If your student needs both renters and auto coverage, ask the provider about bundling options to reduce the overall cost.

What is an ‘additional interest‘ on a student renters policy?

An additional interest is a person or entity listed on the policy to receive updates and notifications, such as cancellation or renewal notices, but who has no coverage under the policy. In student housing, this is commonly a landlord, property management company, or university housing office.

Listing an additional interest is often required in lease agreements. It allows the property owner to confirm that the student has an active renters insurance policy and receive updates if the coverage changes.

This does not give the landlord the right to make claims, change coverage, or receive claim payouts. It is strictly an informational role.

Are sorority or fraternity houses covered?

Coverage for students living in sorority or fraternity houses depends on the structure of the living arrangement. If the house is considered university-owned or affiliated housing, renters insurance may extend to it in the same way it does for a dorm. However, if the house is independently owned or operated by a national organization, it may be treated like any off-campus housing, requiring separate coverage.

Some insurance providers exclude group housing from standard coverage or may impose specific limits.

It is very important to check whether the address is eligible and whether the policy applies to that type of residence.

Students in Greek housing should not assume their belongings are covered unless they confirm the policy terms and list the address specifically.

Can landlords require specific policy terms or limits?

Yes, landlords can require tenants to carry renters insurance and can also set minimum coverage amounts. This is most common in private off-campus housing and student apartment complexes.

Lease agreements may specify:

- Minimum liability coverage (for example, $100,000)

- The landlord or property manager must be listed as an additional interest

- Proof of coverage must be submitted before move-in

Failure to meet these requirements can delay move-in or result in a lease violation. Some landlords even offer renters’ insurance enrollment as part of the leasing process to simplify compliance.

Please encourage your student to read the lease carefully and make sure their policy matches any listed requirements.

Do state laws impact renters’ insurance coverage?

Yes, state laws can influence how renters’ insurance policies are written and what protections are included. Differences may include how liability is handled, what counts as a covered event, or the types of damages that must be disclosed in lease agreements.

For example, in some states, landlords are required to disclose flood risk, while in others, they are not. Certain states may also have rules about liability waivers or restrictions on requiring renters insurance.

Even if the general coverage is the same nationwide, local laws and regional risks, such as wildfires, earthquakes, or hurricanes, can impact policy pricing and what add-ons are available.

If your student is going to college in a different state from your home, it is worth checking the state-specific rules and making sure the policy accounts for those regional differences.

Also Read: Landlord vs. Renters Insurance

Can renters’ insurance affect a student’s credit or rental history?

Renters’ insurance itself does not typically impact credit scores, but the way claims are handled can have longer-term effects. If your student files multiple claims in a short period of time, those may be recorded in a database called the CLUE report (Comprehensive Loss Underwriting Exchange).

Landlords and insurers may use CLUE reports when evaluating future rental applications or new insurance policies. A history of frequent or large claims could raise red flags, even if the student was not at fault.

On the other hand, having an active renters’ insurance policy and not making frequent claims can show responsibility and reduce future insurance costs.

Encourage your student to use renters’ insurance wisely, only for meaningful losses, and to understand that while it offers important protection, claims are recorded and may be reviewed in the future.

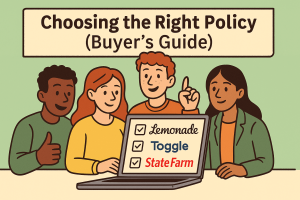

Choosing the Right Policy (Buyer’s Guide)

Not all renters’ insurance policies are created equal. Some are built for speed and simplicity, while others offer more customization or support through a local agent. If you are helping your student choose the right policy, it helps to compare the options side by side.

Below is a breakdown of three popular providers, Lemonade, Toggle, and State Farm that college students commonly use. Each offers a different approach, so the best student renters insurance really depends on your child’s lifestyle, tech comfort, and housing situation.

Lemonade: Fast and Fully Digital

Best for: Tech-savvy students who want instant coverage

Lemonade is known for its sleek mobile app and fast claims process. Your student can sign up in minutes and manage everything from their phone. This provider is popular with students because of its low monthly rates and no-pressure setup. Many policies start around $5 per month, depending on coverage levels and location.

Lemonade uses artificial intelligence to handle most claims quickly. Some claims are processed and paid within a few hours. Coverage includes personal property, liability, and loss of use, with the option to customize based on your student’s needs.

If your student lives in a dorm or small apartment and prefers not to deal with agents or phone calls, Lemonade offers a straightforward path.

Highlights:

- Instant quotes and coverage

- Easy mobile app

- Fast claims process

- No in-person contact required

Toggle: Customizable and Student-Friendly

Best for: Students who want flexibility and modern options

Toggle is a renters insurance brand backed by Farmers Insurance and built with younger renters in mind. What makes Toggle stand out is the flexibility. Students can add coverage for things like electronics, side hustles, and even identity theft protection.

Toggle lets you build a personalized policy that fits different living styles, whether your student is in a traditional dorm, shared apartment, or hybrid housing. Plans start low and can be upgraded easily, depending on how much coverage is needed.

It is especially useful if your student owns items that fall outside basic coverage or wants some extra financial protection beyond the basics.

Highlights:

- Modern coverage options

- Flexible plan builder

- Add-ons for electronics or gig work

- Coverage even in non-traditional student housing

- Many times require Auto Pay

State Farm: Reliable and Agent-Supported

Best for: Parents who want traditional support and bundled policies

State Farm is one of the most recognized insurance companies in the country and is often chosen by families who already have auto or homeowners insurance with them. You can bundle renters’ insurance with an existing policy to receive a discount, and claims can be handled either online or through a dedicated agent.

Coverage is reliable and well-established, making it a strong option if you prefer to speak with a human and want help customizing the right plan. State Farm is also a good choice for students who live off campus and need to meet specific landlord requirements.

Because of the company’s national presence, coverage options and availability are consistent across most states.

Highlights:

- Local agent support available

- Bundle discounts with auto insurance

- Good for families already using State Farm

- Trusted name in property insurance

Choosing What Works for Your Student

Here are a few key questions to help guide the decision:

- Does your student live on or off campus?

- Off-campus housing almost always requires its own policy.

- How valuable are your students’ belongings?

- A basic policy may be enough for dorm life, but shared apartments or students with high-value electronics may need more protection.

- Do you want an agent or a self-serve option?

- Some parents prefer traditional support, while students may lean toward digital-only coverage.

- Is bundling an option?

- If your family already has auto insurance with one of these providers, ask about discounts for adding a renters policy.

Choosing the best student renters’ insurance depends on how your student lives and what type of support you value. Lemonade is great for simplicity. Toggle offers maximum flexibility. State Farm provides long-term stability and agent guidance. No matter which path you choose, having coverage in place before move in day helps protect your student’s belongings and gives both of you peace of mind.

Also Read: Best Renters Insurance for College Students in 2025

Common Mistakes Parents Make

Even with the best intentions, it is easy for parents to overlook small but costly details when it comes to protecting their college student’s belongings. Renters’ insurance is often treated as an afterthought until something goes wrong. Avoiding these common mistakes can save you time, money, and unnecessary stress during the school year.

Assuming Homeowner’s Insurance Automatically Covers Everything

One of the most frequent mistakes is believing that a parent’s homeowner’s policy will cover a student’s belongings at college. While some policies extend limited coverage to dependents living in dorms, that coverage may be capped, excluded by distance, or come with a high deductible. Once your student moves off campus, separate renters’ insurance is typically required.

Always verify the limits and exclusions of your homeowner’s policy before assuming your student is protected.

Waiting Until After Move-In Day

Another mistake is waiting until something happens before looking into coverage. Renters’ insurance needs to be in place before theft, fire, or damage occurs. Once the policy is active, coverage typically begins immediately or within 24 hours.

Setting up renters insurance before your student moves in ensures that their belongings are protected from day one and avoids the panic of trying to rush a policy during an emergency.

Choosing the Wrong Coverage Limits

It is easy to underestimate the value of what your student brings to school. Laptops, phones, musical instruments, clothing, and even small appliances can add up quickly. Choosing the lowest possible coverage limit may not be enough to replace everything after a major loss.

Take a quick inventory with your student and estimate the replacement cost of their belongings. Use that number to choose a realistic personal property limit.

Not Listing the Correct Address

Renters’ insurance policies are tied to a specific physical address. If your student moves mid-year, sublets a different unit, or forgets to update their housing information, their coverage may no longer apply. Claims can be denied if the listed address does not match the actual location of the loss.

Remind your student to update their policy any time they move apartments, switch housing between semesters, or change their living arrangements.

Also, review all documents carefully. Some colleges and universities provide a separate mailing address for students. Be sure to list the physical address where your student actually lives not just the mailing address.

Skipping Liability Coverage

Some families focus only on replacing belongings but overlook liability protection. If your student accidentally causes damage to their unit or injures someone during a visit, they could be held responsible for the costs. Liability coverage helps cover medical expenses, legal fees, and property damage.

It is a vital part of any renters’ insurance policy, even for students who do not own many high-value items.

Avoiding these mistakes starts with being proactive. Renters’ insurance is affordable, flexible, and designed to give you and your student peace of mind. A few small steps now can prevent major headaches later.

Next Steps & Move-In Checklist

Once you have decided that your student needs renters’ insurance, the next step is making sure everything is in place before move-in day. A little preparation now can help avoid surprises later and make the transition smoother for both you and your student.

Below is a simple checklist to walk you through the process of choosing, enrolling in, and confirming student renters insurance. Use it as a guide to stay on track.

✅ Parent-Friendly Student Insurance Checklist

1. Review the housing type

-

- Is your student living in a dorm, an apartment, or a shared house?

- Is the housing on-campus or off-campus?

- Will they be on the lease or subletting?

2. Check existing insurance policies

-

- Review your current homeowner’s insurance to see if it extends any coverage.

- Look for restrictions based on location, distance, or value limits.

- If the student is off-campus, assume they need their own policy.

3. Take inventory of personal belongings

-

- Walk through what your student is bringing: electronics, clothes, textbooks, sports gear, furniture, etc.

- Estimate the replacement value for each major item.

- Use this to set realistic personal property coverage limits.

4. Choose a renters insurance provider

-

- Compare top student-friendly options like Lemonade, Toggle, or State Farm.

- Consider pricing, support options, digital tools, and bundling opportunities.

- Make sure coverage includes personal property, liability, and loss of use.

5. Confirm address and lease information

-

- Use the correct address for your student’s policy.

- If they are subletting or moving between semesters, confirm dates and lease terms.

- Double-check that any landlord or school requirements are met.

6. Set up the policy

-

- Select your desired coverage limits and deductible.

- Add any extras such as coverage for high-value electronics or bikes.

- List the student as the named insured and any required landlord as an additional interest.

7. Save and share documents

-

- Save a digital copy of the insurance policy and ID card.

- Share access with your student in case they need to file a claim.

- Provide documentation to the landlord or housing office if required.

8. Remind your student what is covered

-

- Go over what counts as a covered event and what does not.

- Discuss how to file a claim and when to contact the provider.

- Encourage them to lock up valuables and keep receipts or photos of key items.

Getting renters’ insurance set up is one of the simplest ways to protect your student’s belongings and reduce financial stress. By following this checklist, you can make sure nothing is overlooked and start the school year with peace of mind.

Conclusion

As your student begins this exciting new chapter, there is a lot to think about—classes, roommates, schedules, and independence. But one thing that should not be left to chance is protecting the belongings they rely on every day. A single theft, fire, or accident can quickly lead to stress, financial loss, and disruption in their routine. That is where student renters insurance proves its value.

For just a few dollars a month, renters’ insurance can cover items like laptops, phones, clothes, and textbooks. It can also provide personal liability coverage if your student accidentally damages someone else’s property or causes an injury. Whether they live in a dorm, off-campus apartment, or shared housing, having the right policy in place gives both of you greater peace of mind.

Throughout this guide, we have walked through the questions parents have about what student renters’ insurance covers, how it works, and what to look out for. You now understand why homeowner’s insurance is not always enough, how to compare coverage options, and what steps to take before move-in day.

The next move is simple.

If your student is living away from home this school year, take a few minutes to review your options and secure coverage. You can compare trusted student renters’ insurance providers, get instant quotes, and choose a policy that fits your student’s living situation.